Written by Ron Cooke, President & Founder of Strategic Wealth Protection Partners in Ontario, CEA®, Member of the Estate Planning Council Canada

“How much tax will my estate or beneficiaries pay on my RRSP when I die?”

Your RRSP value is fully taxable in the year of death unless transferred to a spouse or dependent. For large RRSPs, this can push total income into the highest tax bracket, instantly wiping out nearly half the account value.

When you die, your RRSP is treated as if you cashed it out the day before your death.

The full value of the account is added to your final income tax return. That means it’s taxed at your marginal rate, which is the highest rate that applies to your total income that year. The exact rate depends on your total income, where you live, and whether any of the RRSP can be transferred tax-free to a spouse or dependent.

The tax rate on your RRSP at death is the combined federal and provincial tax rate.

The good news is that if you name your spouse or common-law partner as the beneficiary, the RRSP can usually roll over tax-free into their RRSP or RRIF. The same applies to dependent children or grandchildren in certain cases.

But if your RRSP goes to your estate or adult children, it’s fully taxable right away, often creating a large final tax bill.

That’s why it’s important to plan well in advance by updating beneficiary designations, coordinating with your will, and considering estate planning strategies to spread or reduce taxes before death.

Key Points:

- Tax impact magnitude: The RRSP value is fully taxable in the year of death unless transferred to a spouse or dependent. For large RRSPs, this can push total income into the highest tax bracket, instantly wiping out half the account value.

- Timing and liquidity issues: If the RRSP passes to the estate, taxes are due before assets can be distributed—creating cash flow challenges for heirs or executors.

- Rollover opportunities: Spousal and dependent rollovers can defer taxes, while adult children or non-qualified beneficiaries trigger full taxation.

- Proactive strategies: Put in place withdrawal strategies, RRSP-to-RRIF conversions, charitable rollovers, and using life insurance to offset taxes.

Ontario Example

Let’s say you live in Ontario and have:

- $500,000 of other taxable income in the year of death, and

- an RRSP worth $1 million.

Your total taxable income becomes $1.5 million.

Because of Canada’s marginal tax system, part of that income is taxed at lower rates, but the majority of your RRSP would be taxed at the top rate of 53.53% (2025). In this case, if you have not named a spouse, common-law partner, or dependent child as the beneficiary, your estate could owe roughly $500,000 to $520,000 in tax on the RRSP alone, depending on available credits and deductions.

Resources:

- Amounts paid from an RRSP or RRIF upon the death of an annuitant

- Ontario tax rates

- Estate Planning in Ontario

What Happens to Your RRSP When You Die?

When I meet with clients across Ontario, one of the most common questions I hear is, “What happens to my RRSP when I die?”

It’s a fair question, especially when your RRSP or Registered Retirement Income Fund (RRIF) represents one of your largest assets. Understanding how these accounts are taxed and transferred can help your family avoid unpleasant surprises later on.

When someone passes away, the Canada Revenue Agency (CRA) treats their Registered Retirement Savings Plan (RRSP) as if it were sold at fair market value on the date of death. This is called a deemed disposition, and it means the entire balance is included in the deceased’s income for that final year.

The RRSP’s fair market value is determined by your financial institution at death, and this amount is reported on your final tax return. Unless a tax deferral applies, this sum becomes taxable income, which can push your estate into a higher tax bracket and result in significant taxes payable.

Federal Tax Rates in Canada

Federal and provincial income tax rates change every year. To calculate what your RRSP or RRIF might be taxed at, you’ll need to check the latest information on both the Government of Canada and Ontario Ministry of Finance websites.

Remember, your RRSP is subject to both federal and provincial taxation at death.

Resources:

What Happens If Your Spouse Is the Beneficiary?

When your surviving spouse or common-law partner is named as the direct beneficiary of your RRSP, the tax deferral can continue. The plan’s value can transfer directly to your spouse’s RRSP or RRIF without triggering immediate income tax.

This rollover means your spouse can continue growing the funds tax-deferred until withdrawals are made in the future. However, the transfer must occur correctly and within specific CRA time frames to qualify for the deferral.

What Are RRSP Rollovers for Spouses and Dependents?

RRSPs can roll over tax-deferred to more than just a spouse. The CRA also allows special rollovers to:

- A financially dependent child or grandchild, if they were dependent on you due to a disability. In this case, the funds may be transferred into their Registered Disability Savings Plan (RDSP) for continued tax deferral.

- A financially dependent minor child or grandchild, where the funds are used to purchase an annuity that pays out over a fixed period.

These options can preserve family wealth and reduce the taxes payable by spreading the income over time instead of recognizing it all in one year.

Who Is Responsible for Paying the Tax?

If there’s a direct beneficiary named, that person generally receives the full RRSP balance, and the estate becomes responsible for paying the related income tax. The CRA ensures collection by assessing the estate for the deceased’s income, even if the funds were paid directly to someone else.

If there are insufficient assets in the estate to pay the taxes, CRA may seek payment from the beneficiary. This is why careful beneficiary planning and tax projections are essential in estate planning.

What Happens If Your Estate Is the Beneficiary?

When your estate is listed as the beneficiary, the RRSP proceeds flow into your estate account and become part of your overall assets.

While this provides flexibility in distribution, it can also increase probate fees in Ontario and delay payment to heirs, since the funds are included in the estate’s taxable income.

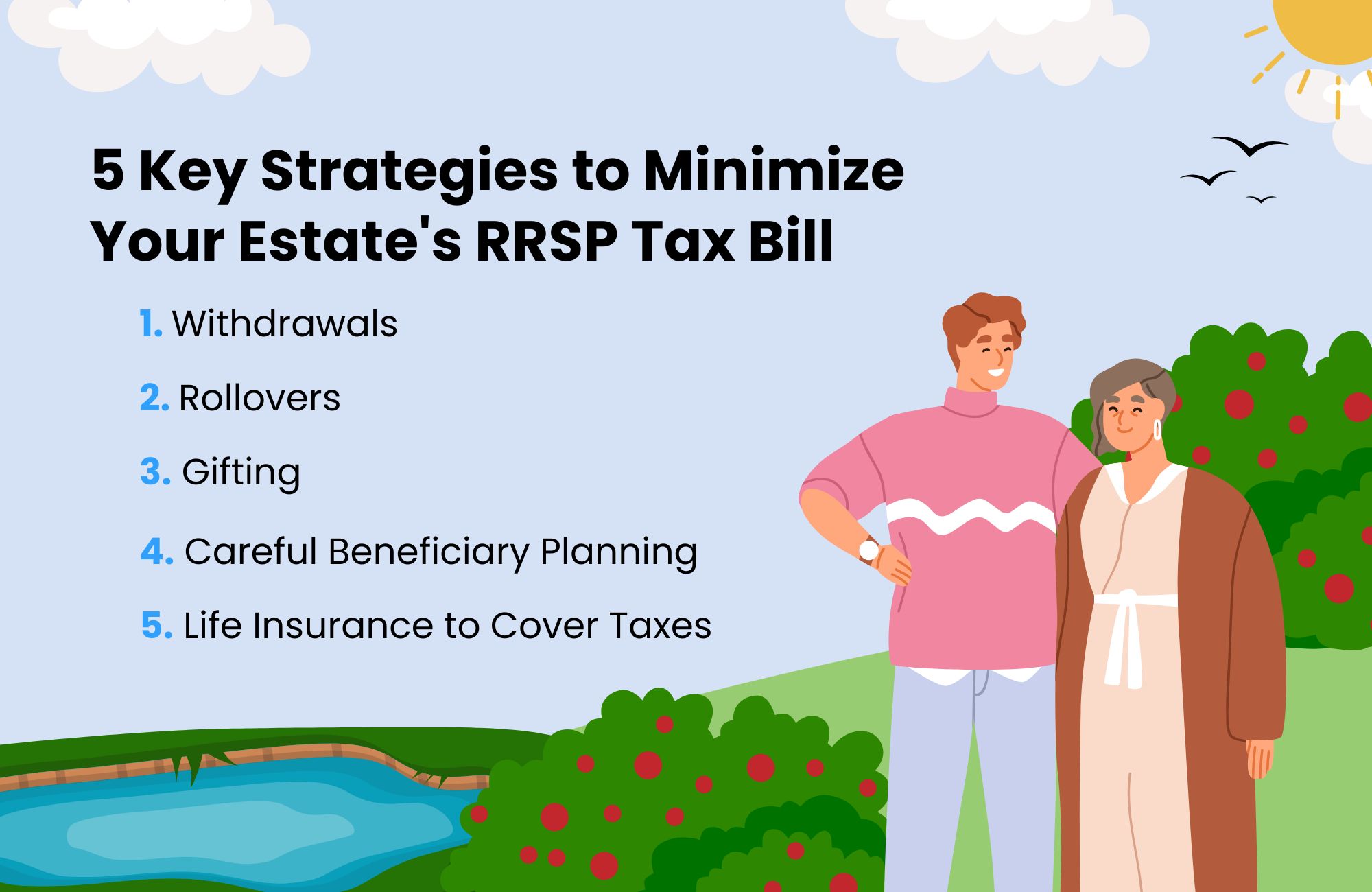

5 Key Strategies to Minimize Your Estate’s RRSP Tax Bill

1. Withdrawals

Strategic withdrawals during retirement can help reduce the size of your RRSP over time, preventing a large tax bill later. Coordinating withdrawals with other income sources ensures you don’t push yourself into a higher tax bracket.

2. Rollovers

Transferring RRSP assets to a spouse or financially dependent child provides valuable tax deferral and may eliminate immediate taxation at death. This ensures more of your savings continue to grow tax-deferred.

3. Gifting

Gifting assets from non-registered accounts while you’re alive can reduce your overall estate value and future taxable income. This strategy can help balance income needs with family generosity.

4. Careful Beneficiary Planning

Naming the right beneficiary and reviewing this regularly can prevent unintended taxes or probate exposure. A qualified estate planner ensures these align with your broader tax and estate goals.

5. Life Insurance to Cover Taxes

Permanent life insurance can provide a tax-free benefit to cover the taxes owing on your RRSP or RRIF. This ensures your heirs don’t need to liquidate investments or property to pay the final bill.

Who Should I Work with to Minimize My Estate’s Tax Bill?

Minimizing the tax impact of your RRSP or RRIF requires coordination between your accountant, financial planner, and estate planning specialist.

If you’re in Ontario, I recommend speaking with our team at SWPP, where we integrate financial planning, taxation, and estate design into one cohesive strategy. If you live outside Ontario, an experienced accountant or estate lawyer can help you navigate the Canada Revenue Agency rules and provincial tax nuances to protect your family’s legacy.

If you are a resident of Ontario, you can work with SWPP. We’re based in Ontario and help Ontario business owners, real estate investors, families, and professionals with tax-smart estate planning and wealth building.

Common Questions

How to avoid tax on a RRIF after death?

You can defer tax by naming your spouse or a financially dependent child as the beneficiary. Otherwise, the full balance becomes taxable in your final return.

Can an RRSP be transferred to a spouse or child upon death?

Yes. A spouse or common-law partner can receive a full tax-deferred rollover. A dependent child may qualify for a partial rollover under specific CRA rules.

Can an RRSP be left to a charity or non-qualified beneficiary?

Yes, but charitable donations must meet CRA criteria. Otherwise, the RRSP value will be taxable to the estate before the donation credit applies.

What is the best way to withdraw from an RRSP without paying tax?

While taxes can’t be avoided entirely, strategic withdrawals, income smoothing, and spousal rollovers can minimize taxable income and reduce the overall tax impact.

💡 Real Case Study: Peter and Jasmine’s Personal Wealth Triangle

When I first met Peter and Jasmine, they were 67 and 63, a wonderful couple who had been married for 35 years.

Peter had sold his business about five years earlier, and together they had built a comfortable life with significant assets: a combined RRSP of about $1.8 million, a non-registered portfolio worth $3.5 million, and a home valued at roughly $2.3 million.

They wanted to understand how to plan their estate and reduce the taxes payable their children would face. After reviewing everything, I saw that their RRSPs were their largest taxable asset, and that continuing to defer taxes would result in a growing liability, a current $963,000 tax bill upon their passing.

To address this, we created a Personal Wealth Triangle. Each year, they withdraw $100,000 from their non-registered portfolio and deposit it into an estate insurance policy. They then assign the policy to a bank, which lends them back the same amount to reinvest in their portfolio.

Because the borrowed money is used for investment, the loan interest is tax deductible.

This allows them to defer tax, preserve their investment base, and create a tax-free estate benefit. Upon their passing, the insurance will pay out approximately $3 million, covering the loan and interest, while still leaving about $1.5 million for their children tax free.

Three years later, Peter and Jasmine are so pleased with the results that they’ve asked about starting a second Personal Wealth Triangle to further enhance their family legacy.

Final Thoughts

RRSPs are one of the most powerful retirement tools in Canada, but without planning, they can also become one of your estate’s largest tax liabilities.

Understanding how tax deferral, income tax, and beneficiary planning work together can make the difference between preserving your wealth or losing a significant portion of it to the CRA.If you’re based in Ontario and you’d like to explore how to align your RRSP and estate plan to reduce taxes and maintain family harmony, book a confidential Ontario estate planning consultation today.

Discover How to Minimize Taxes and Secure Your Legacy

Did you know that without a solid estate plan, taxes and fees in Ontario could claim a significant portion of your wealth?

If you’ve worked hard to build your business, investments, and properties, protecting your legacy for your loved ones is critical. At Strategic Wealth Protection Partners, we specialize in helping high-net-worth individuals in Ontario secure their financial futures.

Our Living Estate Plan is designed to:

- Reduce estate taxes and probate fees.

- Simplify wealth transfer to your loved ones.

- Reflect your values and priorities in every detail.

Your Legacy Matters

With our personalized guidance, we’ll help you navigate options like Living Trusts to protect your assets and ensure your family’s peace of mind. Contact us today to book your Living Estate Plan Consultation and take the first step toward a secure future.

Schedule a Living Estate Plan Consultation

Planning your legacy is about more than numbers—it’s about ensuring your family remembers you and your values are honoured for many years to come.

Estate planning and trusts can feel overwhelming, especially if it’s your first time. That’s why we’re here.

With our simple, 5-Step Living Estate Plan, we make the process easy, helping you create a comprehensive estate plan or trust that protects your assets from taxes and probate fees while preserving your legacy. Tools like The Final Word Journal capture your story, wishes, and essential details like accounts and end-of-life plans, ensuring your family has clarity and comfort.

Take the first step today—schedule a consultation call and give your family the ultimate gift: peace of mind and the assurance they were always your priority.

Read More

If you’re starting your estate planning process, you may find these articles helpful:

- Who Pays Tax on an RRSP at Death?

- What Is the Tax Rate on a RRIF at Death?

- Does a Spouse Automatically Inherit Everything in Ontario?

- How Much Is Estate Tax in Ontario?

- Is a Life Insurance Payout Taxable in Canada?

About the Author

RON COOKE, PRESIDENT & FOUNDER OF STRATEGIC WEALTH PROTECTION PARTNERS

With over 30 years in financial services, I’ve seen the challenges families face when a loved one passes—lost assets, unnecessary taxes, and emotional stress. That’s why I created the Living Estate Plan, a comprehensive process to protect assets, eliminate estate and probate fees, and create legacies that are remembered for many years to come.

This plan ensures your family receives not just your wealth, but a meaningful reminder of your care and love. Tools like The Final Word Journal capture your story, wishes, and essential details, offering clarity and comfort during difficult times.

Your final gift should be more than money—it should be peace of mind, cherished memories, and an organized estate.

Schedule a Call

Schedule a 30-minute consultation call with Strategic Wealth Protection Partners.

Click HERE to schedule a consultation.