Written by Ron Cooke, President & Founder of Strategic Wealth Protection Partners in Ontario, CEA®, Member of the Estate Planning Council Canada

Is life insurance worth it?

Life insurance is often worth it if you have people who depend on your income, you own a business, or you want to protect your estate. The value depends on your financial goals, life stage, and whether the structure of your policy aligns with those goals.

Keep reading to find out when life insurance is worth it in Canada. There isn’t a simple clear-cut answer.

Table of Contents

- Do You Need Life Insurance?

- Quick Checklist: Is Life Insurance Worth It for You?

- Pros and Cons of Life Insurance in Canada

- Who Benefits Most from Life Insurance?

- Types of Life Insurance: Term vs Permanent

- Comparing Term vs Permanent Insurance with Examples

- How Policy Ownership Affects Value and Control

- Using Permanent Life Insurance as a Financial Tool

- How Life Insurance Fits Into Estate Planning in Ontario

- How Much Life Insurance Do You Need?

- What Does Life Insurance Cost in Canada?

- When You Might Not Need Life Insurance

- How to Choose a Life Insurance Provider

- Alternatives to Life Insurance

- FAQ

Do You Need Life Insurance?

Imagine the financial pressure your loved ones could face if something unexpected happened.

From mortgage payments to final expenses, life insurance fills the financial gap when you’re no longer there to provide.

If you have a spouse, kids, or aging parents who rely on your income, life insurance ensures they can maintain financial stability if you pass away. It can also cover funeral expenses, repay debts, and provide peace of mind during an already difficult time.

Even if you’re single, a small policy can help cover your final expenses or leave a gift to someone important to you. For business owners, life insurance can protect partners, keep operations running, and help fund succession plans.

But, if no one relies on you financially and you have enough saved to cover your debts and funeral costs, you may not need life insurance right now.

Quick Checklist: Is Life Insurance Worth It for You?

Ask yourself:

- Do you have a spouse, partner, or dependents who rely on your income?

- Would your family struggle financially if you died?

- Do you have debts like a mortgage, car loan, or business loan?

- Do you want to help cover funeral costs or taxes owed by your estate?

- Are you a business owner or someone with significant assets?

- Are you planning to leave an inheritance?

- Are you young and healthy enough to get a low premium?

If you answered “yes” to any of these, life insurance is worth exploring.

Pros and Cons of Life Insurance in Canada

Life insurance provides peace of mind, but it’s important to weigh the benefits and costs.

Pros

- Protects your family financially if you die

- Helps cover debts, funeral costs, or major expenses

- Offers a tax-free lump sum to beneficiaries

- Can fund business buyouts or key person replacement

- Some policies build cash value over time

- Helps with estate planning and wealth transfer

- Premiums are lower when purchased young

Cons

- Can be expensive, especially with permanent policies

- Not always necessary for single people with no dependents

- Term policies expire, and permanent ones are complex

- Medical exams or underwriting may be required

- Group or mortgage insurance may provide similar coverage but often has limitations, such as lack of portability or declining benefits

Who Benefits Most from Life Insurance?

| Group | Pros | Cons |

| Young Families | Protects kids and spouse, replaces income | May not use policy if term ends early |

| Seniors | Helps cover final taxes, leaves a legacy | Higher premiums, fewer term options |

| Business Owners | Covers loans, supports succession planning | Requires proper structuring, legal advice |

| Single Adults | Covers debts, funeral, or legacy gift | Might not be needed if no financial dependents |

| Real Estate Investors | Pays off property debt, aids estate planning | Can duplicate coverage without coordination |

| Estate Planners | Helps equalize inheritance, pays estate taxes | Costly if started late in life |

Types of Life Insurance: Term vs Permanent

There are two main types of life insurance:

Term Life Insurance

- Covers you for a set period (e.g., 10, 20, or 30 years)

- Pays a lump sum if you die during the term

- Ideal for covering temporary needs like a mortgage or raising children

- Cheaper but has no cash value

- Expires at end of term unless renewed (at a higher cost)

Permanent Life Insurance

- Covers you for your entire life

- Includes cash value that grows over time

- Can be used for estate planning, retirement income, or emergencies

- More expensive up front but lower cost over several decades of coverage and guarantees a payout

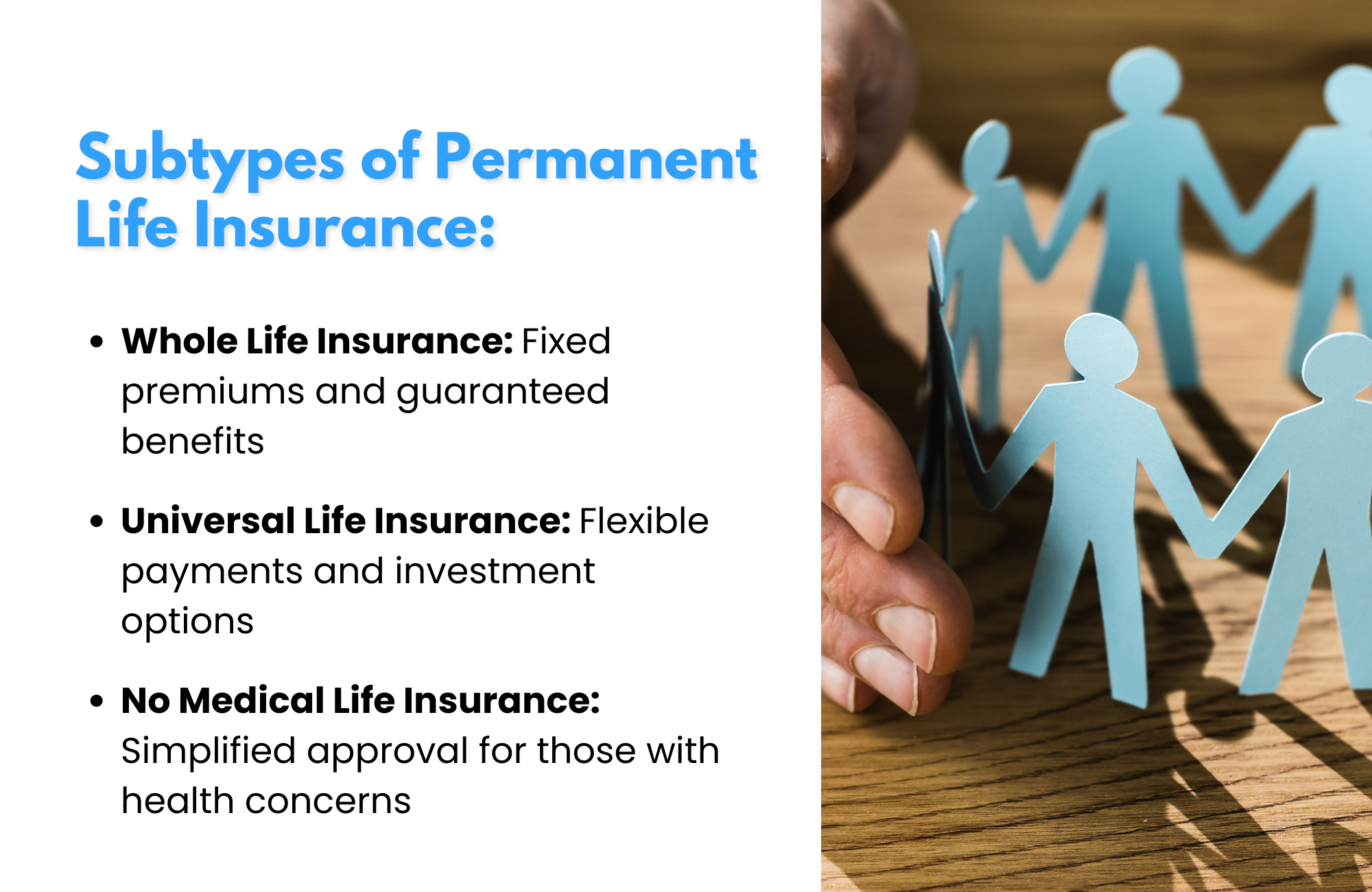

Subtypes of Permanent Life Insurance:

- Whole Life Insurance: Fixed premiums and guaranteed benefits

- Universal Life Insurance: Flexible payments and investment options

- No Medical Life Insurance: Simplified approval for those with health concerns

Comparing Term vs Permanent Insurance with Examples

Example 1: Young Family – Term Policy

A 35-year-old parent buys a $500,000, 20-year term policy to cover the mortgage and raise children. If they die during the term, the payout helps keep the family financially stable.

Example 2: Business Owner – Term Policy

A small business owner uses a 10-year policy to match a loan repayment period. If they pass away, the death benefit repays the loan and protects the business.

Example 3: Estate Planning – Permanent Policy

A 60-year-old purchases a $1M whole life policy to cover final taxes and ensure equal inheritance among children. The cash value also grows tax-deferred.

Example 4: Retirement Strategy – Permanent Policy

A 45-year-old builds up cash value in a universal life or whole life policy and later borrows against it tax-free to help supplement retirement.

How Policy Ownership Affects Value and Control

Who owns the policy determines who controls it—and who may be taxed.

This is a complex topic covered here in brief. Make sure you speak with your broker to understand how policy ownership will affect your life insurance, particularly in terms of taxation.

Personally-Owned Policies

- Most common type for individuals and families

- Owner controls the policy and names beneficiaries

- Death benefit is typically paid tax-free to beneficiaries (not the estate)

- The owner can access or borrow against the policy’s cash value, if applicable.

Joint Ownership (e.g., Spouses)

- Typically “first-to-die” or “last-to-die” structures

- First-to-die means the policy pays out when the first person dies, providing immediate financial support to the surviving spouse or family.

- Last-to-die pays out only after both people have passed, and is often used to cover estate taxes or leave an inheritance.

- A good fit for couples with shared financial responsibilities or long-term estate planning needs.

- Joint policies with named beneficiaries usually avoid probate, which can help simplify estate settlement and reduce delays.

Corporate-Owned Policies

- Business owns and pays for the policy

- Corporation receives the death benefit tax-free

- Part of the benefit can be paid to shareholders tax-free via the Capital Dividend Account (CDA)

- Any remaining payout may be taxable if not structured properly

- The corporation controls access to the policy’s cash value and may use it as collateral for loans.

Ontario Tip: Corporate-owned insurance can also fund buy-sell agreements and replace key individuals, but must be carefully designed to ensure CRA compliance.

Note: Changing the policy’s ownership later on can trigger taxes or loss of control—speak with an advisor before making changes.

Using Permanent Life Insurance as a Financial Tool

Permanent life insurance can be more than just protection—it can build value.

Cash Value Access

- You can borrow against the policy’s value without triggering tax, as long as the policy remains active

- Withdrawals may be taxed if they exceed your adjusted cost basis (ACB)

Example: A 45-year-old real estate investor in Ontario owns a portfolio of rental properties generating steady income. They hold a universal life insurance policy with a $500,000 death benefit, which has accumulated $200,000 in cash value after 15 years of premiums.

To seize an opportunity to purchase a $300,000 investment property, they take a $100,000 policy loan against the cash value at a low interest rate. The loan is tax-free under CRA rules, as it’s considered a borrowing against the policy, not income, and requires no immediate repayment.

They use the loan as a down payment, combining it with a mortgage for the balance. The rental income from the new property covers the loan’s interest and mortgage payments, preserving their cash flow. If the loan remains unpaid at their death, the $100,000 (plus accrued interest) will reduce the death benefit paid to their beneficiaries.

Meanwhile, all the policy’s cash value continues to grow tax-deferred, offering future liquidity for additional investments or retirement planning.

How Life Insurance Fits Into Estate Planning in Ontario

Life insurance is a strategic estate planning tool, especially in Ontario where probate fees apply.

- Helps cover Estate Administration Tax (1.5% on assets over $50,000)

- Provides liquidity to pay final taxes, avoiding forced sales of property

- Can equalize inheritances between children

- Avoids probate delays when a beneficiary is named directly

- Can fund charitable gifts and leave a legacy

Example: A 55-year-old Toronto resident owns a $2M home, $1.5M in investment accounts (e.g., stocks and RRSPs), and has two adult children. Their estate, valued at $3.5M, faces Ontario’s Estate Administration Tax (approximately 1.5% on assets over $50,000, or about $51,750) and potential income taxes on RRSPs if not rolled over to a spouse. To ensure liquidity and avoid forced asset sales, they purchase a $1M whole life insurance policy.

The policy’s tax-free death benefit provides immediate funds to cover probate fees, final income taxes, and a $200,000 charitable gift to a local hospital. By naming their children as beneficiaries, the payout bypasses the estate, avoiding probate delays and ensuring an equitable inheritance. The policy’s cash value also grows tax-deferred, offering flexibility for future financial needs.

How Much Life Insurance Do You Need?

A common rule is 10–15x your annual income, but your actual needs depend on:

- Mortgage or rent

- Other debts (loans, credit cards, taxes)

- Childcare or education expenses

- Final expenses and estate taxes

- Your spouse’s ability to earn income

Online calculators can help—but talking to an advisor ensures you don’t over- or under-insure.

What Does Life Insurance Cost in Canada?

Pricing varies depending on your age, health, smoking status, and the type of policy you choose.

To give you a general sense, the table below shows estimated monthly premiums for a $500,000 life insurance policy—a common amount that many Canadians choose to help cover a mortgage, family expenses, or final taxes.

This comparison includes both term life insurance (which covers you for a fixed number of years) and permanent life insurance (which lasts your entire life and may include a cash value component).

Keep in mind that rates will vary between insurers and policy features. This table is a very general overview.

| Age | Term Policy ($500,000) | Permanent Policy ($500,000) |

| 30 | $20–$30/month | $200–$400/month |

| 45 | $40–$60/month | $400–$600/month |

| 60 | $100+/month | $800+/month |

Permanent policies are more costly, but offer lifetime coverage and investment features.

When You Might Not Need Life Insurance

You may not need coverage if:

- You’re single with no debt or dependents

- Your estate has enough liquid assets to cover taxes and expenses

- You’re retired and no longer earning income

- Your workplace plan is sufficient for your goals

Even so, it’s wise to review your needs every few years as life changes.

How to Choose a Life Insurance Provider

Look for:

- Strong financial strength ratings (e.g., AM Best, DBRS)

- Easy-to-understand policy terms and riders

- Affordable premiums with flexible payment options

- Online tools and responsive support

- Advisors who can explain how life insurance fits into estate or business planning

Alternatives to Life Insurance

Life insurance isn’t for everybody. Here are some examples of alternatives to life insurance you may wish to consider:

| Alternative | How It Works | Best For |

| Emergency Fund | Covers short-term expenses from savings | Singles or minimal debt |

| TFSA/RRSP | TFSA passes tax-free; RRSP taxed unless rolled over | Long-term savers |

| Real Estate | Can be sold to fund estate or passed to heirs | Property owners |

| Business Succession Plan | Built-in agreements to protect partners | Entrepreneurs |

| CPP Death Benefit | Government payout (max $2,500) | Low-income or retirees |

FAQ

Is it better to save money or buy life insurance?

Both saving and life insurance are essential parts of a healthy financial plan. Life insurance provides instant protection for your loved ones if you die, while saving builds long-term wealth and flexibility.

Can life insurance help create financial security for my family?

Yes. Life insurance gives your family a financial safety net, helping them manage living costs, debts, or education if you’re no longer around to provide.

Do you receive money from life insurance?

Yes. When the insured person passes away, their beneficiary receives a death benefit—typically a tax-free lump sum payment.

What is a life insurance death benefit and how does it compare to a payout?

They are the same thing. The “death benefit” is simply the technical name for the life insurance payout your beneficiary receives.

What does life insurance cover?

Life insurance covers financial needs that arise when someone dies—like funeral costs, mortgage payments, debt, or lost income for dependents.

How much life insurance coverage do I need?

A common rule of thumb is to get coverage equal to 10–15 times your annual income, plus any debts and future expenses such as children’s education or final taxes.

What are typical term life premiums in Canada?

For a healthy 30-year-old, a 20-year term policy with $500,000 in coverage may cost between $20 and $40 per month, depending on the insurer and policy details.

What makes permanent life insurance policies different from term life insurance policies?

Permanent life insurance offers lifelong coverage and includes a cash value component that grows over time. Term life insurance is more affordable and covers a set period, such as 10, 20, or 30 years.

What is whole life insurance?

Whole life is a type of permanent insurance with fixed premiums, guaranteed coverage for life, and a cash value that grows tax-deferred. It’s often used in estate or legacy planning.

How does the cash value component of a permanent life insurance policy work?

The cash value is a built-in savings feature that grows inside the policy. You can borrow against it or withdraw funds, although taxes may apply if you take out more than your policy’s cost basis.

How does life insurance support financial planning?

Life insurance protects your financial plan by ensuring debts, final expenses, and income replacement are covered. Permanent policies can also grow wealth tax-efficiently and be used as part of estate or business planning.

Is life insurance different in Ontario?

The basics of life insurance are consistent across Canada, but Ontario has unique estate considerations like probate fees. This makes policy structure and beneficiary designations especially important in Ontario-based financial planning.

Final Thoughts

Life insurance is more than a safety net—it’s a cornerstone of a solid financial and estate plan.

Whether you’re protecting a young family, securing a business, or planning your legacy, the right policy helps you do it confidently.

In Ontario, smart structuring can reduce probate, lower taxes, and ensure your heirs receive what you’ve worked hard to build. The key is knowing what type of insurance you need—and getting the right advice to make it work for you.

Discover How to Minimize Taxes and Secure Your Legacy

Did you know that without a solid estate plan, taxes and fees in Ontario could claim a significant portion of your wealth?

If you’ve worked hard to build your business, investments, and properties, protecting your legacy for your loved ones is critical. At Strategic Wealth Protection Partners, we specialize in helping high-net-worth individuals in Ontario secure their financial futures.

Our Living Estate Plan is designed to:

- Reduce estate taxes and probate fees.

- Simplify wealth transfer to your loved ones.

- Reflect your values and priorities in every detail.

Your Legacy Matters

With our personalized guidance, we’ll help you navigate options like Living Trusts to protect your assets and ensure your family’s peace of mind. Contact us today to book your Living Estate Plan Consultation and take the first step toward a secure future.

Schedule a Living Estate Plan Consultation

Planning your legacy is about more than numbers—it’s about ensuring your family remembers you and your values are honoured for many years to come.

Estate planning and trusts can feel overwhelming, especially if it’s your first time. That’s why we’re here.

With our simple, 5-Step Living Estate Plan, we make the process easy, helping you create a comprehensive estate plan or trust that protects your assets from taxes and probate fees while preserving your legacy. Tools like The Final Word Journal capture your story, wishes, and essential details like accounts and end-of-life plans, ensuring your family has clarity and comfort.

Take the first step today—schedule a consultation call and give your family the ultimate gift: peace of mind and the assurance they were always your priority.

Read More

If you’re starting your estate planning process, you may find these articles helpful:

- Is Life Insurance Taxable in Canada?

- Probate Fees Ontario: How to Calculate and Plan for Probate

- Can I Write My Own Will in Ontario?

About the Author

RON COOKE, PRESIDENT & FOUNDER OF STRATEGIC WEALTH PROTECTION PARTNERS

With over 30 years in financial services, I’ve seen the challenges families face when a loved one passes—lost assets, unnecessary taxes, and emotional stress. That’s why I created the Living Estate Plan, a comprehensive process to protect assets, eliminate estate and probate fees, and create legacies that are remembered for many years to come.

This plan ensures your family receives not just your wealth, but a meaningful reminder of your care and love. Tools like The Final Word Journal capture your story, wishes, and essential details, offering clarity and comfort during difficult times.

Your final gift should be more than money—it should be peace of mind, cherished memories, and an organized estate.

Schedule a Call

Schedule a 30-minute consultation call with Strategic Wealth Protection Partners.

Click HERE to schedule a consultation.