Written by Ron Cooke, President & Founder of Strategic Wealth Protection Partners in Ontario, CEA®, Member of the Estate Planning Council Canada

Is Life Insurance Taxable in Canada?

Is life insurance taxable? Life insurance payouts are generally not taxable in Canada if they are paid directly to a named beneficiary.

However, taxation may apply in certain scenarios involving estate payouts, business ownership, policy loans, or withdrawals. Understanding ownership and structure is key to avoiding tax traps.

Make sure you speak with your insurance broker to get a clear picture of how your life insurance will be taxed. But for a general breakdown, keep reading to find out which scenarios may result in a tax hit.

Table of Contents

- What Is Life Insurance and How Does It Work in Canada?

- How Are Life Insurance Payouts Made?

- How Does Policy Ownership Affect Taxation?

- What Happens If You Borrow Against Your Life Insurance?

- When Is Life Insurance Taxable in Canada?

- When Is Life Insurance Not Taxable?

- Are Policy Loans Taxable if the Policy Is Lapsed or Surrendered?

- How to Structure Your Policy to Minimize Tax

- How Life Insurance Supports Estate Planning in Ontario

- FAQ

- Do I Need Life Insurance? (Self-Assessment)

- Final Thoughts

What Is Life Insurance and How Does It Work in Canada?

Life insurance is a contract between you and an insurance company that pays a death benefit to your chosen beneficiary when you pass away.

It’s designed to provide financial support to your family or dependents and can be an important part of estate planning.

There are two main types of life insurance in Canada:

- Term Life Insurance: Term life insurance offers coverage for a specific period (e.g., 10, 20, or 30 years). If you pass away during that period, your beneficiary receives the death benefit. If you outlive the term, the policy ends with no payout.

- Permanent Life Insurance: This type of insurance offers lifelong coverage and builds cash value over time. You can access this cash value while you are alive, which can add flexibility—but may trigger tax consequences.

How Are Life Insurance Payouts Made?

When the insured person passes away, the insurance company pays out a death benefit:

- A lump-sum payment is usually made to the named beneficiary after the company receives a completed claim form and a death certificate.

- If no beneficiary is named, the death benefit is paid to the deceased’s estate, which can cause delays and increase tax exposure due to probate.

- Payments are generally received within a few weeks, though this can vary depending on circumstances.

Ontario Tip: In Ontario, if the payout goes to the estate, it may be subject to Estate Administration Tax (commonly called probate), which can cost approximately 1.5% of the estate’s value.

How Does Policy Ownership Affect Taxation?

The ownership of a life insurance policy in Canada significantly affects taxation.

We can’t cover every possible scenario in this article, so this is a general overview of how policy ownership affects taxation. Speak to your insurance broker, financial advisor, or accountant to find out more about how your life insurance policy will be taxed.

Personally-Owned Policies

How do personally-owned policies work?

- Death benefit is generally tax-free to named beneficiaries.

- Withdrawals or surrenders may be taxed if they exceed adjusted cost base.*

- Policy loans may be partially taxable if the loan exceeds the policy’s adjusted cost base or triggers a policy disposition. A policy disposition is any event that causes a life insurance policy to be partially or fully terminated for tax purposes in Canada.

- If the beneficiary is the estate, the death benefit could be subject to probate and affect the overall estate tax burden.

- Personally-owned policies do not have access to the Capital Dividend Account** (CDA), so the death benefit cannot be paid out to heirs tax-free through a corporation.

Joint Policies (e.g., spouses)

How do joint-owned policies work?

- Usually structured as “first-to-die” or “last-to-die.”

- First-to-die pays out upon the first death. Common for income replacement or estate equalization.

- Last-to-die pays after both insureds have passed. Often used for estate planning, since tax liabilities typically arise at the second death.

- Tax rules depend on how premiums are paid and by whom.

- If jointly owned, the surviving owner retains the policy without triggering tax.

- If owned by one spouse, there may be probate or tax implications depending on beneficiary designation.

- Withdrawals from policies with a cash value (e.g., joint last-to-die whole life) can be taxable if they exceed the policy’s adjusted cost base.

- Last-to-die policies are often used to fund future tax liabilities (e.g., capital gains on a cottage or business) with lower premiums than two single policies.

- If structured correctly under provincial law, some jointly owned policies may offer protection from creditors.

Corporate-Owned Policies

How do corporate-owned policies work?

- Business pays the premiums and is usually the beneficiary.

- Death benefit is paid tax-free to the corporation.

- Only the portion of the payout above the adjusted cost base can be paid to shareholders tax-free through the CDA. The CDA calculation involves subtracting the adjusted cost base from the death benefit. Improper structuring could lead to part of the proceeds being treated as a taxable dividend when paid out to shareholders.

- Any remaining balance is taxable if distributed.

- Premiums are not tax-deductible in most cases, unless the policy is collateral for a business loan and specific conditions are met.

*Adjusted Cost Base: In the context of life insurance, the Adjusted Cost Base (ACB) refers to the running total of the premiums paid into a life insurance policy, adjusted over time for certain tax-related additions or subtractions. It’s used by the Canada Revenue Agency to determine how much of a policy’s cash value or payout is taxable if it’s accessed or transferred.

**Capital Dividend Account: The Capital Dividend Account (CDA) is a special account that exists only on a private Canadian corporation’s books. It’s not a bank account—it’s a tax tool that lets the corporation pay certain tax-free dividends to its shareholders. When the CDA has a positive balance, the corporation can pay tax-free dividends to Canadian shareholders. If a life insurance policy is owned by a corporation and someone insured dies, part of the death benefit can often go into the CDA, making it possible to pass money to shareholders without triggering personal tax.

General Small Business Owner Example:

A 50-year-old co-owner of an Ontario-based manufacturing company, valued at $3M, shares the business equally with a partner.

To ensure business continuity if either passes away, they establish a buy-sell agreement funded by a corporate-owned $1.5M whole life insurance policy, with the company as the beneficiary.

If one owner dies, the tax-free death benefit is paid to the corporation, enabling it to buy out the deceased’s shares from their estate at fair market value. The payout, less the policy’s adjusted cost base, is credited to the Capital Dividend Account (CDA), allowing tax-free dividends to be paid to the surviving owner’s shares.

This structure avoids probate, ensures a smooth transition, and minimizes tax liability, provided the policy and agreement are properly structured with legal and tax advice.

Ontario Business Note: Many Ontario-based business owners use corporate-owned life insurance in buy-sell agreements or key-person planning. These strategies require detailed structuring to remain tax-efficient.

Consult a tax professional or estate planning expert for complex corporate or estate planning scenarios.

What Happens If You Borrow Against Your Life Insurance?

You can borrow against the cash value of a permanent life insurance policy. This is treated as a loan, not income, which usually means no immediate tax.

Types of Loans:

1) Policy Loans (from the insurer)

- No tax unless the policy lapses or is surrendered with the loan unpaid.

- Interest accrues but doesn’t affect tax unless the policy ends.

2) Third-Party Loans (bank loans secured against policy)

- Common in “insured retirement” strategies.

- Interest may be deductible if used for investment or business purposes.

- Policy must remain active; if it lapses, a taxable gain may occur.

Example: Jane uses her permanent policy’s $200,000 cash value to secure a $150,000 line of credit for a real estate investment. No tax is triggered unless she surrenders the policy or dies before repaying the loan.

When Is Life Insurance Taxable in Canada?

While most life insurance payouts are not taxable, certain actions, ownership structures, or beneficiary designations can change this.

These tables are general in nature and don’t cover every possible scenario. Make sure you speak with your broker to find out how your life insurance will be taxed in Canada.

Common Taxable Situations:

| Situation | Why It’s Taxable | Ownership Context |

|---|---|---|

| Death benefit is paid to the estate | Becomes part of the estate and may face probate fees and taxes | Personal or joint-owned, if no named beneficiary or if the estate is the beneficiary |

| Withdrawals from a permanent policy exceed premiums paid | The amount over the adjusted cost base is taxed as income | Personal or joint-owned, less common in corporate-owned policies |

| Surrendering a policy for its cash value | Any gain above the adjusted cost base is considered income | Any ownership, but most common with personal or corporate policies |

| Interest earned on a delayed payout | The interest portion is taxable as income | Usually personal or joint-owned (corporate payouts are rarely delayed) |

| Policy is used as collateral for a loan | If the policy lapses or is surrendered with an unpaid loan, the amount exceeding the adjusted cost base may be taxed as income, particularly for corporately owned policies | Applies to corporate and personal ownership; tax impact depends on structure |

| Dividends taken in cash from a participating policy | These are taxable unless left to grow within the policy | Applies to personal or corporate policies with participating whole life |

| Selling a life insurance policy | This may result in a taxable capital gain or income event | Applies to personal and corporate ownership, but rare in both |

Note: Most of these scenarios apply to personally or jointly owned policies, but some (like collateral loans or corporate beneficiaries) also apply to corporate-owned life insurance. Ownership type can significantly affect taxation—especially when dealing with loans, CDA credits, or estate inclusion.

When Is Life Insurance Not Taxable?

| Situation | Why It’s Not Taxable | Ownership Context |

|---|---|---|

| Paid directly to a named individual | CRA treats it as a non-taxable event | Applies to personally or jointly owned policies with a named beneficiary who is not the estate |

| Policy cash value remains untouched | Grows tax-deferred inside the policy | Applies to personal, joint, or corporate-owned policies |

| Loans are repaid and policy remains in force | Loans are not income; no tax applies unless policy lapses | Applies to personal, joint, or corporate-owned policies |

| Benefit is paid to a registered charity | May provide tax credits or deductions for the estate | Applies to personally owned policies where the charity is owner, beneficiary, or both |

| Beneficiary is a spouse or child | Personal policies allow tax-free transfer in most cases | Applies to personally owned policies only; corporate policies don’t pass to family members without tax unless structured separately |

Note: Most tax-free scenarios apply to personally or jointly owned policies with clear beneficiary designations. Corporate-owned policies follow different rules—particularly when transferring funds to shareholders or family members.

Are Policy Loans Taxable if the Policy Is Lapsed or Surrendered?

Yes.

If the policy ends while a loan is still outstanding, and the loan exceeds the policy’s adjusted cost base, the excess is taxed as income.

Example: You borrow $80,000 from your policy with $5,000 in accrued interest. If your adjusted cost base (ACB) is $60,000 and the policy lapses, you could be taxed on the $25,000 difference ($80,000 loan + $5,000 interest – $60,000 ACB)

This is often overlooked and can result in a surprise tax bill.

How to Structure Your Policy to Minimize Tax

- Name a specific beneficiary to avoid routing payouts through your estate

- Avoid naming minors directly; use a trust to hold the benefit

- Review corporate policies annually to ensure proper CDA use

- Coordinate with your estate plan, especially if you hold high-value assets

Work with a licensed estate planner or insurance advisor who understands Ontario tax law.

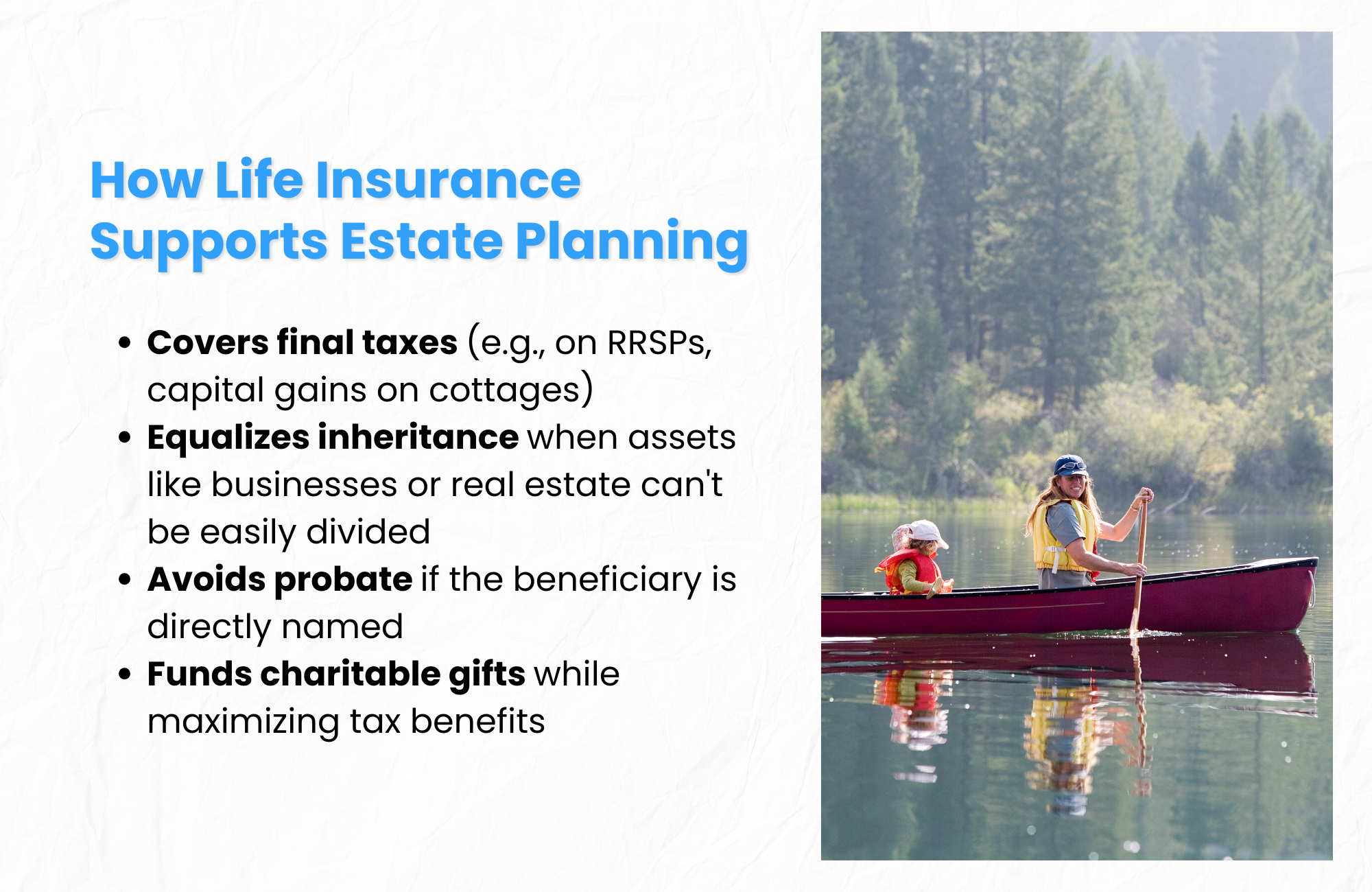

How Life Insurance Supports Estate Planning in Ontario

Life insurance plays a key role in estate planning:

- Covers final taxes (e.g., on RRSPs, capital gains on cottages)

- Equalizes inheritance when assets like businesses or real estate can’t be easily divided

- Avoids probate if the beneficiary is directly named

- Funds charitable gifts while maximizing tax benefits

Ontario-Specific Example: Let’s say a Toronto resident owns a $2 million home and leaves it to one child. To equalize their estate, they buy a $2 million life insurance policy and name their other child as beneficiary. This avoids selling assets and keeps their estate balanced.

FAQ

What are the income tax consequences of surrendering a life insurance policy?

If you surrender your permanent policy, any amount above your adjusted cost base is considered income. That excess is taxable whether the policy is personally or corporately owned.

What are the tax implications of naming your estate as the beneficiary?

The payout may face probate fees and taxes in Ontario. It can also be used to pay estate debts, delaying inheritance distribution.

Is a death benefit taxable in Canada?

Generally, death benefits are not taxed if paid to a named beneficiary. If paid to the estate, taxes or probate may apply.

Are life insurance premiums tax-deductible?

Premiums are not deductible for individuals. Businesses may deduct premiums under specific conditions, such as when the policy is used as collateral for a loan for income-producing purposes, like key-person insurance.

What happens if no beneficiary is named?

The payout will go to your estate and may face delays, taxes, and probate. This can reduce what heirs ultimately receive.

Is the cash surrender value taxable?

Yes, the amount above your policy’s adjusted cost base is considered income. That portion is subject to income tax in the year it’s received.

Is life insurance considered an asset?

Permanent policies with cash value are assets and may be included in estate valuations. Term policies are not classified this way.

Should I buy from a broker or insurer?

Brokers provide more choice and personalized advice.

Do I Need Life Insurance?

Self-Assessment

Final Thoughts

While life insurance payouts are generally tax-free, many Canadians get caught by avoidable tax traps related to ownership, loans, and estate planning.

Whether you're protecting your family or funding your business succession plan, structuring your policy the right way is crucial.

In Ontario, probate fees and final tax bills can significantly affect your estate. By planning ahead, naming beneficiaries properly, and using expert guidance, you can maximize the value of your life insurance and protect what matters most.

Discover How to Minimize Taxes and Secure Your Legacy

Did you know that without a solid estate plan, taxes and fees in Ontario could claim a significant portion of your wealth?

If you’ve worked hard to build your business, investments, and properties, protecting your legacy for your loved ones is critical. At Strategic Wealth Protection Partners, we specialize in helping high-net-worth individuals in Ontario secure their financial futures.

Our Living Estate Plan is designed to:

- Reduce estate taxes and probate fees.

- Simplify wealth transfer to your loved ones.

- Reflect your values and priorities in every detail.

Your Legacy Matters

With our personalized guidance, we’ll help you navigate options like Living Trusts to protect your assets and ensure your family’s peace of mind. Contact us today to book your Living Estate Plan Consultation and take the first step toward a secure future.

Schedule a Living Estate Plan Consultation

Planning your legacy is about more than numbers—it’s about ensuring your family remembers you and your values are honoured for many years to come.

Estate planning and trusts can feel overwhelming, especially if it’s your first time. That’s why we’re here.

With our simple, 5-Step Living Estate Plan, we make the process easy, helping you create a comprehensive estate plan or trust that protects your assets from taxes and probate fees while preserving your legacy. Tools like The Final Word Journal capture your story, wishes, and essential details like accounts and end-of-life plans, ensuring your family has clarity and comfort.

Take the first step today—schedule a consultation call and give your family the ultimate gift: peace of mind and the assurance they were always your priority.

Read More

If you’re starting your estate planning process, you may find these articles helpful:

- Is Life Insurance Worth It in Canada? Pros & Cons

- When You Inherit a House in Ontario, Is It Taxable?

- Death Tax Canada: How to Avoid a Surprise Tax Hit

About the Author

RON COOKE, PRESIDENT & FOUNDER OF STRATEGIC WEALTH PROTECTION PARTNERS

With over 30 years in financial services, I’ve seen the challenges families face when a loved one passes—lost assets, unnecessary taxes, and emotional stress. That’s why I created the Living Estate Plan, a comprehensive process to protect assets, eliminate estate and probate fees, and create legacies that are remembered for many years to come.

This plan ensures your family receives not just your wealth, but a meaningful reminder of your care and love. Tools like The Final Word Journal capture your story, wishes, and essential details, offering clarity and comfort during difficult times.

Your final gift should be more than money—it should be peace of mind, cherished memories, and an organized estate.

Schedule a Call

Schedule a 30-minute consultation call with Strategic Wealth Protection Partners.

Click HERE to schedule a consultation.