Written by Ron Cooke, President & Founder of Strategic Wealth Protection Partners in Ontario, CEA®, Member of the Estate Planning Council Canada

“What tax implications will my beneficiaries face when I die?”

When you pass away, your RRSP is treated as if you cashed it out the day before your death.

This is called a deemed disposition. The full fair market value of your RRSP is added to your final income tax return, which can create a big tax bill.

However, there are important exceptions. If your spouse, common-law partner, or a financially dependent child or grandchild is the beneficiary, the RRSP can usually roll over to them tax-free. That means they don’t pay tax right away.

Instead, the money just moves into their RRSP or RRIF, and taxes are deferred until they withdraw the funds later.

If you name your estate or someone else (like an adult child who isn’t dependent), the RRSP value is taxed in your final return, and your estate pays the tax before distributing what’s left.

Naming the right beneficiary can significantly reduce taxes and make things easier for your family.

Key Points:

- Naming a qualified beneficiary, planning RRSP withdrawals before death, and aligning RRSP strategy with your estate or corporate plan can significantly reduce overall taxes.

- On death, the full value of the RRSP is taxed as income unless transferred to a qualified beneficiary such as a spouse, common-law partner, or dependent child/grandchild.

- A spousal or dependent child/grandchild rollover allows the RRSP to transfer tax-free, deferring taxes until the beneficiary withdraws the funds later.

- Naming your estate as the RRSP beneficiary usually triggers immediate taxation and can increase probate fees and administrative delays.

- When a beneficiary lives outside Canada, RRSP withdrawals are subject to withholding tax (typically 25%) and must be reported in both countries.

What Happens to Your RRSP When You Die?

When someone passes away, one of the most common questions families face is what happens to their Registered Retirement Savings Plan (RRSP).

For many people in Ontario, it’s one of their largest assets, and understanding how it’s taxed after death can make a big difference in how much their loved ones actually receive.

When you die, the Canada Revenue Agency (CRA) applies what’s called a deemed disposition rule. This means your RRSP is treated as if you sold all your investments at their fair market value immediately before death. The total value is then added to your deceased’s final tax return as income.

Unless a tax deferral applies, this can create a large tax bill for your estate.

Are RRSPs Taxed After Death?

Yes. When you pass away, the full fair market value of your RRSP is included in your deceased’s final income tax return.

It becomes part of your taxable income for that year and is subject to both federal and provincial tax rates.

If your RRSP balance is significant, it can push your estate into the highest tax bracket, resulting in a large amount of income tax payable.

In Ontario, this can mean nearly half of your RRSP value goes to taxes unless it qualifies for a rollover or tax deferral.

Who Gets Your RRSP When You Die?

Who receives your RRSP depends on your designated beneficiary or, if none is listed, your estate.

A surviving spouse, common-law partner, or financially dependent child or grandchild can generally receive the proceeds directly, often with more favourable tax and estate planning results.

If no beneficiary is named, the RRSP becomes part of your estate, potentially increasing probate fees and delaying access for your loved ones.

Do Beneficiaries Pay Taxes on RRSPs?

The income tax implications for RRSP beneficiaries depend on who they are and how the transfer is handled.

If your surviving spouse or eligible dependent receives the RRSP through a qualifying rollover, they can often defer tax until they withdraw the funds later.

If the beneficiary is not a qualified person, such as an adult child who is not financially dependent, the entire RRSP amount is taxable to the estate. In this case, the estate pays the tax, not the individual beneficiary.

📖 Read More: Who Pays Tax on an RRSP at Death

How Do Taxes Work for Qualified and Non-Qualified Survivors?

In Ontario, the tax consequences differ depending on who inherits the RRSP.

- A spouse or common-law partner qualifies for a full tax-deferred rollover to their own RRSP or Registered Retirement Income Fund (RRIF).

- A financially dependent child or grandchild may also receive tax-deferred treatment if they meet CRA conditions.

- Any other non-qualified individual will not benefit from a rollover, the RRSP is fully taxable to the estate at death.

Proper tax and estate planning can help ensure your beneficiaries receive the most tax-efficient outcome possible.

How Do You Roll Over an RRSP After Death?

Rolling over an RRSP to a spouse, common-law partner, or dependent child or grandchild allows the funds to remain sheltered under a new RRSP or RRIF in the recipient’s name. To qualify for tax deferral, the rollover must occur by direct transfer and be completed within specific time limits set by the CRA.

The result is that the deceased’s RRSP is not immediately taxed, and the beneficiary continues to enjoy the benefits of tax-deferred growth until they withdraw the funds.

Designating RRPS Beneficiaries

Why Should You Designate an RRSP Beneficiary?

Naming a designated beneficiary on your RRSP simplifies estate administration and helps your loved ones access the funds quickly. It can also bypass probate, reducing probate fees and avoiding delays caused by estate settlement.

How Can You Designate an RRSP Beneficiary?

You can name a beneficiary directly on your RRSP account with your financial institution or through your Will. Keeping this information up to date is essential, especially after major life events such as marriage, divorce, or the birth of children.

A properly structured designation ensures your assets pass smoothly to the intended recipient and minimizes unnecessary income tax implications.

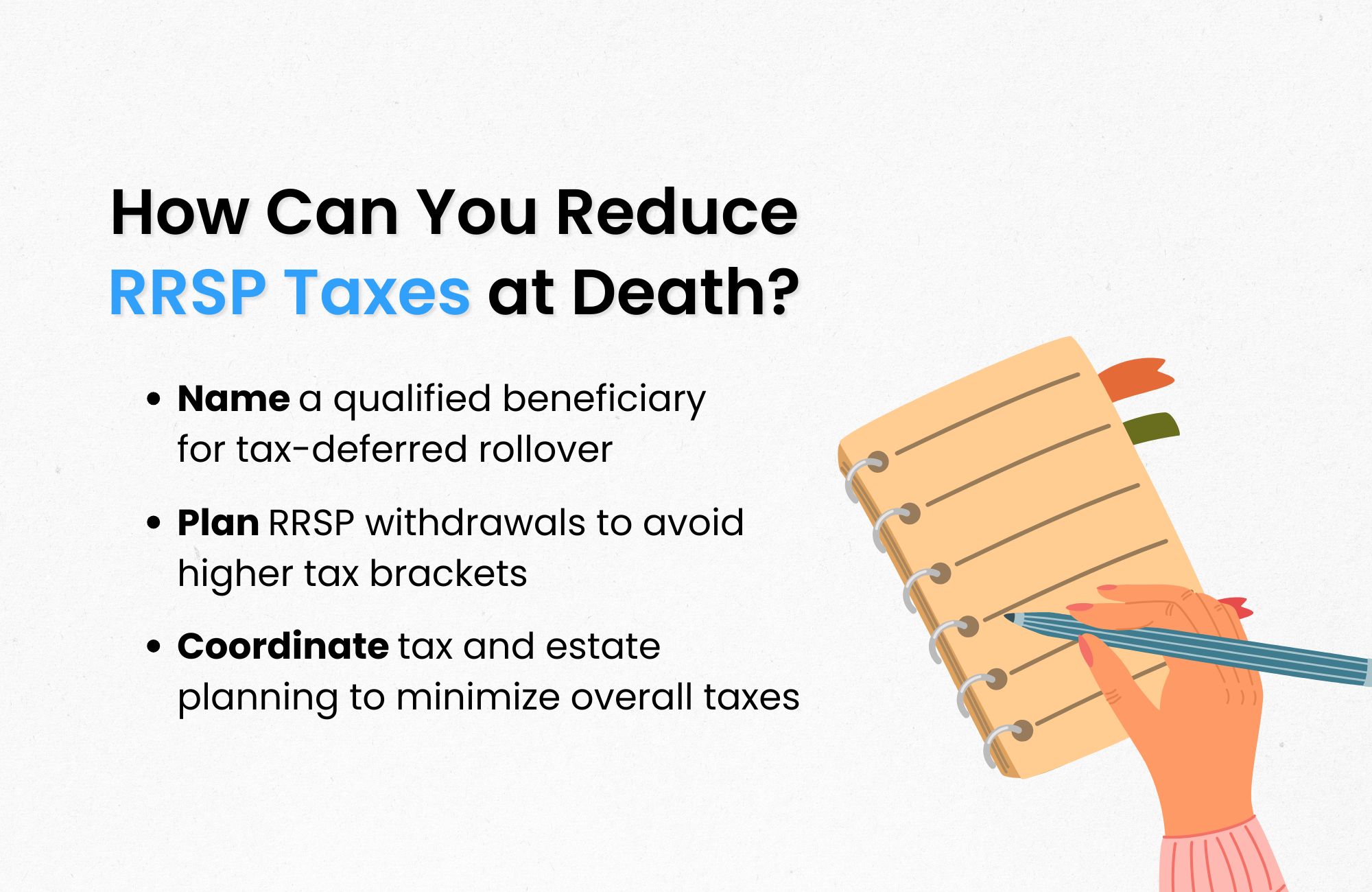

How Can You Reduce RRSP Taxes at Death?

There are several strategies to reduce the tax consequences of RRSPs after death:

- Name a qualified beneficiary, such as a surviving spouse or dependent child, to allow a tax deferral rollover.

- Plan RRSP withdrawals strategically in retirement to spread out taxable income and avoid large tax brackets in later years.

- Coordinate your tax and estate planning so your registered and non-registered assets work together to minimize taxes and maintain family wealth.

Even small planning steps can make a meaningful difference in the taxes your family will owe.

Common Questions

Yes. If your spouse or financially dependent child qualifies, the RRSP can transfer directly to them, allowing a tax deferral until future withdrawals.

Income earned between the date of death and final payout is taxable to the beneficiary, not to the deceased’s estate.

A matured RRSP has already been converted into a Registered Retirement Income Fund (RRIF), while an unmatured RRSP is still in accumulation. Both are subject to similar taxation at death.

Non-resident beneficiaries may face Canadian withholding tax on RRSP proceeds, and they should seek professional advice to understand their income tax implications.

The RRSP value becomes part of the estate, subject to probate fees and taxed on the deceased’s final tax return.

It’s a tax deferral mechanism that allows a spouse or dependent to transfer RRSP assets into their own registered plan without immediate tax.

If you’re a qualified beneficiary, the tax can be deferred. If not, the estate pays the income tax when the RRSP is collapsed.

The funds go directly to the beneficiary, bypassing the estate, but taxes may still apply depending on their eligibility for rollover.

Yes. A charitable donation can offset the taxes owing on the RRSP, but it must be structured properly to ensure full credit.

An RRSP beneficiary receives the plan’s proceeds, while a successor holder (for a RRIF) takes over the account itself, maintaining tax deferral and income continuity.

Final Thoughts

Your RRSP represents years of disciplined saving and planning.

Without the right tax and estate planning, that nest egg could face heavy income tax implications after death, leaving less for your loved ones. By naming the right designated beneficiary and understanding the CRA’s rules for tax deferral, you can preserve more of what you’ve built.

The key is coordination. Make sure your RRSP, RRIF, and other assets work together in a way that protects your family and minimizes taxes.

Discover How to Minimize Taxes and Secure Your Legacy

Did you know that without a solid estate plan, taxes and fees in Ontario could claim a significant portion of your wealth?

If you’ve worked hard to build your business, investments, and properties, protecting your legacy for your loved ones is critical. At Strategic Wealth Protection Partners, we specialize in helping high-net-worth individuals in Ontario secure their financial futures.

Our Living Estate Plan is designed to:

- Reduce estate taxes and probate fees.

- Simplify wealth transfer to your loved ones.

- Reflect your values and priorities in every detail.

Your Legacy Matters

With our personalized guidance, we’ll help you navigate options like Living Trusts to protect your assets and ensure your family’s peace of mind. Contact us today to book your Living Estate Plan Consultation and take the first step toward a secure future.

Schedule a Living Estate Plan Consultation

Planning your legacy is about more than numbers—it’s about ensuring your family remembers you and your values are honoured for many years to come.

Estate planning and trusts can feel overwhelming, especially if it’s your first time. That’s why we’re here.

With our simple, 5-Step Living Estate Plan, we make the process easy, helping you create a comprehensive estate plan or trust that protects your assets from taxes and probate fees while preserving your legacy. Tools like The Final Word Journal capture your story, wishes, and essential details like accounts and end-of-life plans, ensuring your family has clarity and comfort.

Take the first step today—schedule a consultation call and give your family the ultimate gift: peace of mind and the assurance they were always your priority.

Read More

If you’re starting your estate planning process, you may find these articles helpful:

- When You Inherit a House in Ontario, Is It Taxable?

- How Much Can You Inherit Without Paying Taxes In Canada?

- How to Avoid Inheritance Tax on a House in Canada

- How Do I Avoid Capital Gains Tax on Inherited Property in Canada?

- Can I Gift a House to My Son or Daughter Without Paying Taxes in Canada?

About the Author

RON COOKE, PRESIDENT & FOUNDER OF STRATEGIC WEALTH PROTECTION PARTNERS

With over 30 years in financial services, I’ve seen the challenges families face when a loved one passes—lost assets, unnecessary taxes, and emotional stress. That’s why I created the Living Estate Plan, a comprehensive process to protect assets, eliminate estate and probate fees, and create legacies that are remembered for many years to come.

This plan ensures your family receives not just your wealth, but a meaningful reminder of your care and love. Tools like The Final Word Journal capture your story, wishes, and essential details, offering clarity and comfort during difficult times.

Your final gift should be more than money—it should be peace of mind, cherished memories, and an organized estate.

Schedule a Call

Schedule a 30-minute consultation call with Strategic Wealth Protection Partners.

Click HERE to schedule a consultation.