Written by Ron Cooke, President & Founder of Strategic Wealth Protection Partners in Ontario, CEA®, Member of the Estate Planning Council Canada

Who Is Responsible for Paying Tax on an RRSP at Death?

In Canada, when the RRSP account holder dies, the value of the RRSP is generally included in their income for the year of death and taxed on their final return.

The deceased’s estate pays the tax on the RRPS.

However, tax can be deferred if the RRSP is transferred to a qualified beneficiary, such as a spouse or common-law partner or a financially dependent child or grandchild, in certain circumstances.

In those cases, the beneficiary becomes responsible for taxes when they withdraw the funds.

Key Takeaways

- RRSPs are taxed as income at death unless transferred to a qualified beneficiary

- Naming a beneficiary can help avoid probate and reduce tax

- Only certain people qualify for a tax deferral rollover

- RRSPs with no beneficiary are taxed and go through the estate

- RRSP planning should be included in your Will and estate plan

Many people want to know if their loved ones will get the full value of an RRSP after they die, or if there will be a big tax bill left behind.

In this blog, we’ll break down exactly how RRSPs are taxed when someone passes away.

We’ll cover who is responsible for paying those taxes and what steps you can take to help protect your family and your legacy. If you have substantial assets and a large RRSP account, I recommend you schedule a call with an SWPP estate planning expert who can help you minimize taxes.

📖 Related Read: How to Avoid Inheritance Tax in Canada

What Happens to Your RRSP When You Die?

According to Stats Canada, 6.3 million Canadians contributed to an RRSP in 2023.

The majority of contributors were between 45 and 64 years old. This means that over 16% of Canadians contributed to RRSPs. While saving money for retirement is great, many Canadians don’t realize that their RRSP represents a large tax liability upon death.

What Happens to a Registered Retirement Savings Plan (RRSP) After Death in Ontario?

When an RRSP holder passes away in Ontario, the value of the account doesn’t vanish, it becomes part of their estate, and depending on the setup, it can trigger significant tax liability or allow for tax deferral.

If a Designated Beneficiary Is Named

If the designated beneficiary is a surviving spouse or common law partner, the RRSP can transfer directly to them without immediate tax. This tax-deferred rollover means no taxes owing at death; the funds move into their RRSP or RRIF and are only taxed when withdrawn later.

This also avoids probate fees, since the RRSP bypasses the estate.

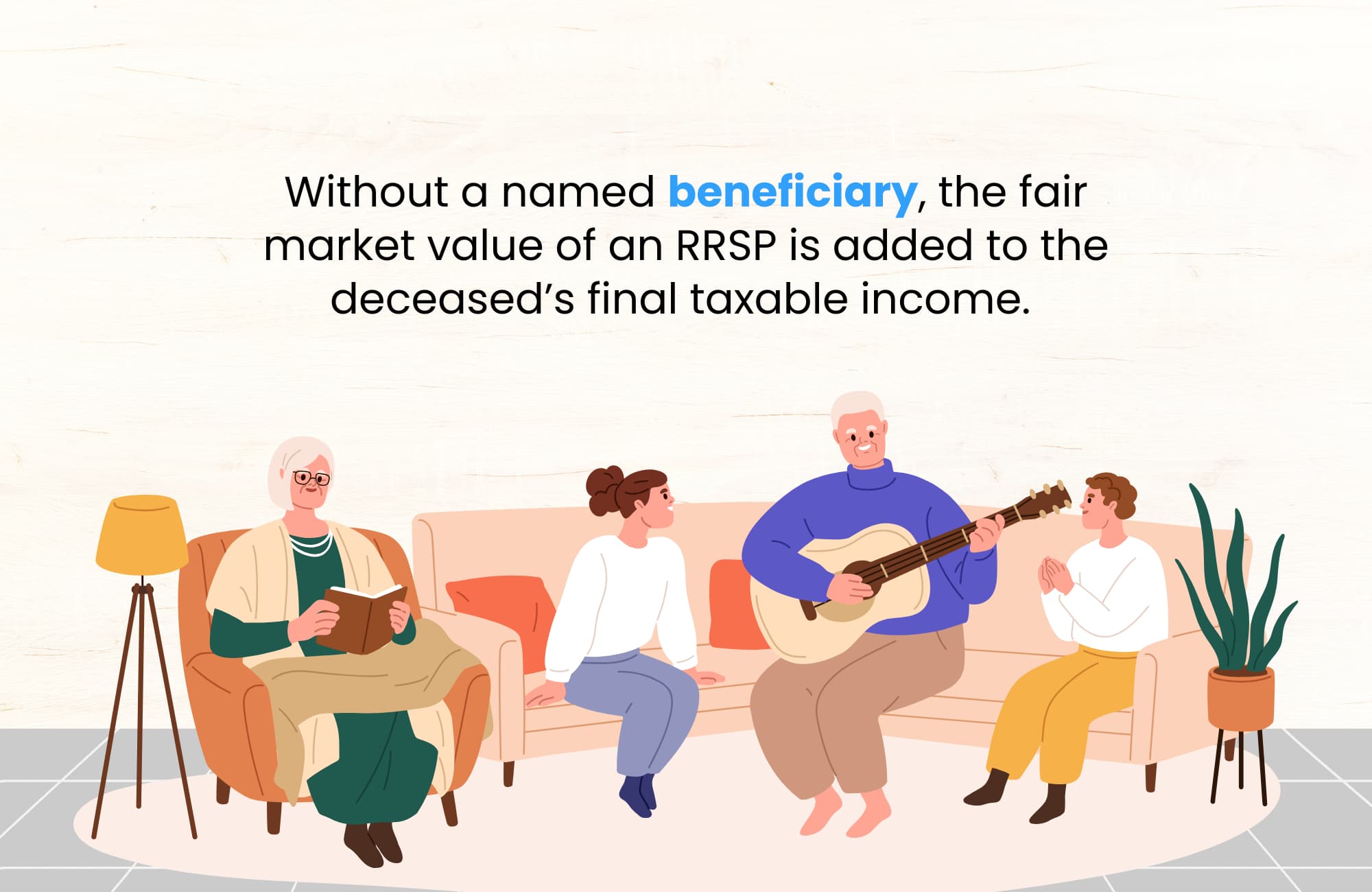

If No Beneficiary Is Named

Without a named beneficiary, the fair market value of the RRSP is added to the deceased’s final taxable income. The estate pays the tax, which can push it into a higher tax bracket. Additionally, probate fees will apply, reducing the amount that ends up with heirs.

There may also be taxes withheld, but these are often not enough to cover the full amount due.

Planning Tips to Reduce the Tax Hit

- Name a surviving spouse or common law partner as designated beneficiary to enable tax deferral

- Keep beneficiary designations up to date, RRSPs don’t automatically follow your will

- Understand how taxable income at death can impact your estate’s bottom line

Thoughtful planning can prevent unnecessary taxes owing and ensure your RRSP supports the people you care about, not just the CRA.

How Are RRSPs Taxed at Death in Canada?

When someone passes away, the full fair market value of their registered retirement savings plan (RRSP) is included in their final taxable income, which can lead to a significant tax liability.

Unless the RRSP is transferred to a surviving spouse, common law partner, or a financially dependent child or grandchild, this amount is treated as income on the deceased’s final return, and taxes owing are paid by the estate. If a qualified designated beneficiary is named, the RRSP can roll over on a tax deferral basis, avoiding immediate taxation.

Without this rollover, taxes withheld may apply, but they often fall short of the actual tax due. Careful estate planning helps reduce the overall impact of these taxes.

How Are RRIFs Taxed at Death in Canada?

When someone dies with a registered retirement income fund (RRIF), its entire fair market value is usually included as taxable income on their final return, unless transferred to a surviving spouse, common law partner, or qualifying designated beneficiary.

This often results in a significant tax liability, as the RRIF is treated as fully cashed out at death.

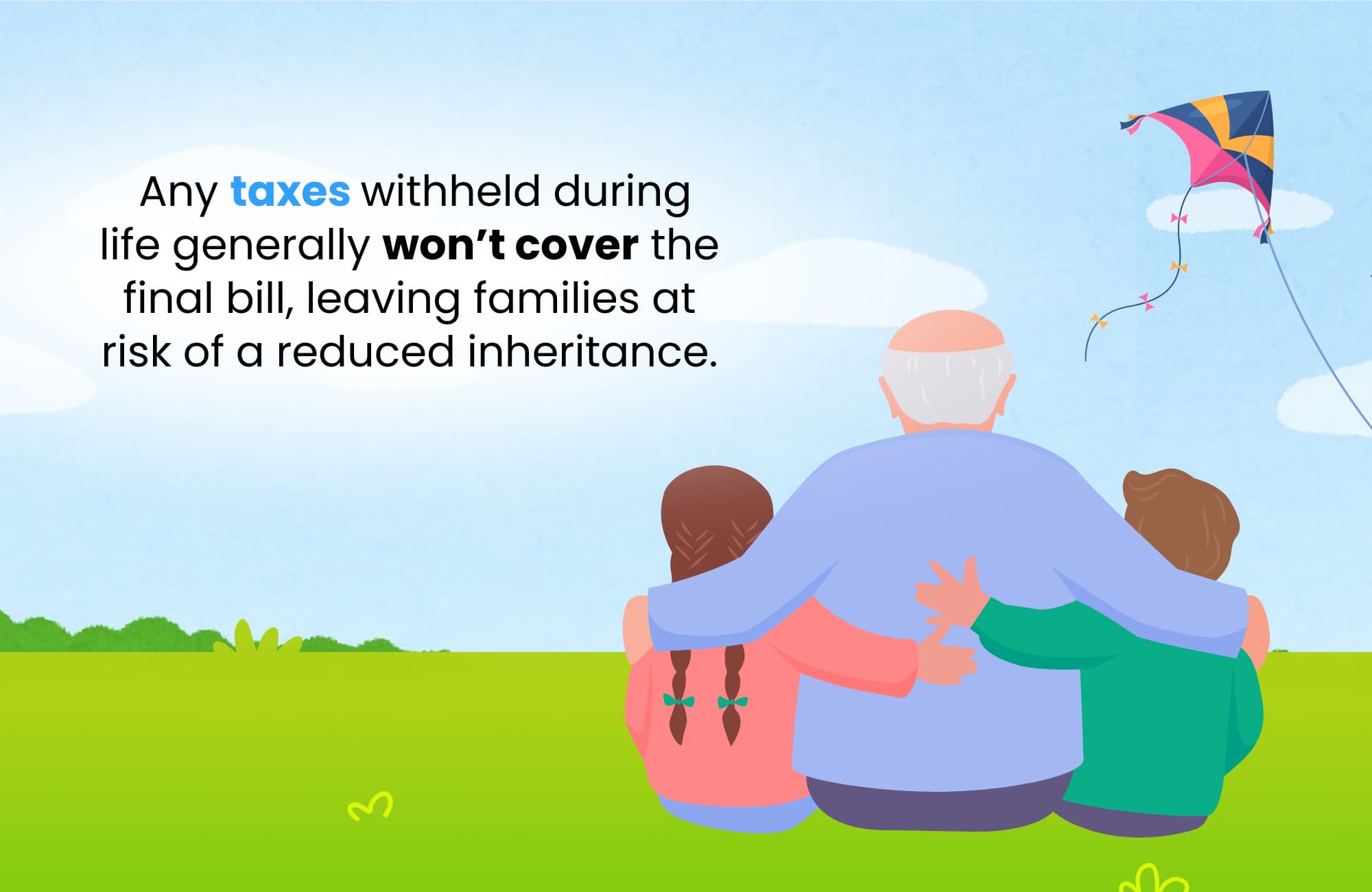

If the RRIF passes to someone other than a qualified beneficiary, the taxes owing must be paid by the estate. While some tax deferral options exist, they are limited and require specific beneficiary relationships. Any taxes withheld during life generally won’t cover the final bill, leaving families at risk of a reduced inheritance.

Table: How Are RRSPs vs RRIFs Taxed at Death?

| Feature | RRSP | RRIF |

|---|---|---|

| Taxable at Death? | Yes | Yes |

| Eligible for Rollover? | Yes | Yes |

| Slips Issued | T4RSP | T4RIF |

| Withholding Tax? | No (on death) | No (on death) |

| Default Tax Impact | Full inclusion in income | Full inclusion in income |

What Happens If the Estate Is the Beneficiary?

When a registered retirement savings plan (RRSP) has no named designated beneficiary, the full fair market value of the plan is paid to the deceased’s estate and reported as taxable income on the final return.

This triggers a potentially large tax liability, as the RRSP is considered fully withdrawn at death. While this may seem simple on the surface, it often leads to higher taxes owing, increased probate fees, and delays in distribution.

Probate is required, which adds costs and reduces the net inheritance. The estate—not a specific person—ends up bearing the weight of both taxation and administration.

Who Pays the Tax on RRSP Proceeds?

If there’s no qualified designated beneficiary, the deceased person’s estate must pay the tax.

The full amount of the RRSP is included in the deceased’s final return, and the Canada Revenue Agency issues a T4RSP slip to the estate, reporting the income.

However, if a qualifying person is named directly on the account, they receive the funds and may also receive the tax slip, depending on whether a tax deferral applies. Who receives the slip determines who bears the tax liability. Getting this wrong can cost families thousands.

What Is an RRSP Rollover and How Does It Work?

An RRSP rollover is a way to defer taxes at death by transferring the value of a deceased person’s RRSP to a qualifying surviving spouse, common law partner, or dependent child or grandchild.

Instead of recognizing the full amount as taxable income right away, the government allows the account to be transferred into another tax-sheltered plan, such as a registered retirement savings plan or registered retirement income fund, in the name of the recipient.

This allows the family to postpone the taxes owing, sometimes for decades. Without the rollover, the tax is immediate, final, and often much higher.

Who Qualifies for a Tax-Free Rollover?

A tax-deferred rollover is available when the RRSP or RRIF is transferred to a:

- Surviving spouse or common law partner

- Dependent child or grandchild who is financially dependent due to a disability

These individuals can shelter the assets inside their own RRSP or RRIF, avoiding immediate tax and preserving wealth for the future.

How to Reduce the Tax Bill on RRSPs at Death

While RRSPs help reduce tax during life, they often create large tax liabilities at death.

Smart planning reduces the burden. You can name a designated beneficiary who qualifies for a tax deferral, use withdrawals strategically in lower-income years, or consider converting the RRSP to a registered retirement income fund earlier than required to smooth the tax impact.

Charitable giving, life insurance, and trusts can also play a role in offsetting the final tax bill. The goal is always to prevent the estate from paying more than it has to.

Why Naming a Beneficiary Is So Important

Without a named designated beneficiary, the RRSP or RRIF will go to the estate, which means probate fees, delays, and higher taxes owing.

But with the right beneficiary named directly on the account, the asset bypasses probate and may qualify for a tax deferral. This simple step can protect family wealth, avoid administrative headaches, and provide faster access to funds during a difficult time. It’s one of the most overlooked but powerful tools in estate planning.

Planning Ahead for RRSP Taxes in Your Will

Too often, families discover too late that RRSP taxes weren’t planned for.

Naming a beneficiary isn’t enough—you also need to consider how taxes withheld, probate, and taxable income from other sources will interact. Your Will should align with your RRSP designations and clearly direct how taxes owing will be handled.

Coordinating your Will with your tax and estate plan helps reduce surprises, keeps things fair, and gives your family peace of mind when they need it most.

Common Questions about Tax on RRSPs after Death

Will I pay taxes as an RRSP beneficiary?

If you’re a qualifying beneficiary, the RRSP can transfer tax-deferred. Otherwise, taxes may be paid by the estate or by you.

What happens to an RRSP at age 71?

It must be converted to a registered retirement income fund or annuity, or fully withdrawn by the end of that year.

Do beneficiaries owe taxes on RRSPs?

Only if the RRSP is paid directly to them and they are not a qualified rollover recipient. Otherwise, the estate usually pays.

What happens to a deceased’s RRSP under the Income Tax Act if there are no beneficiary designations?

The full RRSP value becomes taxable income to the estate and is subject to both income tax and probate fees.

Who has to file the deceased’s income tax return?

The executor or estate trustee is responsible for filing the final return and paying any taxes owing from the estate assets.

Discover How to Minimize Taxes and Secure Your Legacy

Did you know that without a solid estate plan, taxes and fees in Ontario could claim a significant portion of your wealth?

If you’ve worked hard to build your business, investments, and properties, protecting your legacy for your loved ones is critical. At Strategic Wealth Protection Partners, we specialize in helping high-net-worth individuals in Ontario secure their financial futures.

Our Living Estate Plan is designed to:

- Reduce estate taxes and probate fees.

- Simplify wealth transfer to your loved ones.

- Reflect your values and priorities in every detail.

Your Legacy Matters

With our personalized guidance, we’ll help you navigate options like Living Trusts to protect your assets and ensure your family’s peace of mind. Contact us today to book your Living Estate Plan Consultation and take the first step toward a secure future.

Schedule a Living Estate Plan Consultation

Planning your legacy is about more than numbers—it’s about ensuring your family remembers you and your values are honoured for many years to come.

Estate planning and trusts can feel overwhelming, especially if it’s your first time. That’s why we’re here.

With our simple, 5-Step Living Estate Plan, we make the process easy, helping you create a comprehensive estate plan or trust that protects your assets from taxes and probate fees while preserving your legacy. Tools like The Final Word Journal capture your story, wishes, and essential details like accounts and end-of-life plans, ensuring your family has clarity and comfort.

Take the first step today—schedule a consultation call and give your family the ultimate gift: peace of mind and the assurance they were always your priority.

Read More

If you’re starting your estate planning process, you may find these articles helpful:

- Estate Planning Ontario: A Simple Guide to Getting It Right

- Inheritance Tax Ontario: Everything You Need to Know

- What Is the Final Tax Return After Death in Canada?

- How Much Money Can Be Legally Given to a Family Member as a Gift in Canada?

About the Author

RON COOKE, PRESIDENT & FOUNDER OF STRATEGIC WEALTH PROTECTION PARTNERS

With over 30 years in financial services, I’ve seen the challenges families face when a loved one passes—lost assets, unnecessary taxes, and emotional stress. That’s why I created the Living Estate Plan, a comprehensive process to protect assets, eliminate estate and probate fees, and create legacies that are remembered for many years to come.

This plan ensures your family receives not just your wealth, but a meaningful reminder of your care and love. Tools like The Final Word Journal capture your story, wishes, and essential details, offering clarity and comfort during difficult times.

Your final gift should be more than money—it should be peace of mind, cherished memories, and an organized estate.

Schedule a Call

Schedule a 30-minute consultation call with Strategic Wealth Protection Partners.

Click HERE to schedule a consultation.